Credit Control – The importance to your organisation

In this blog, we aim to explain the importance of credit control in Credit Management.

What is Credit Control?

Credit control is about safeguarding the investment the business makes in its Accounts Receivable ledger. It intends to maximise returns from customers who have been supplied on credit terms and are yet to pay, in a way that best supports the business.

When asked to describe credit control, most people think of collections work, which is crucially important. However, it encompasses other important aspects such as risk assessment, customer relationship management, recoveries and legal proceedings, in addition to chasing overdue payments.

Additionally, In larger organisations, there may be specific subject matter experts who handle each component. Whereas, in a smaller business a sole-charge credit controller might be responsible for the entire cycle.

Don't just take it from us - but take it from the CICM Community

Before we get into some of our reasons why Credit Control is so important, take a look at some of the great responses to our Linkedin Post about Credit Control regarding this crucial business function.

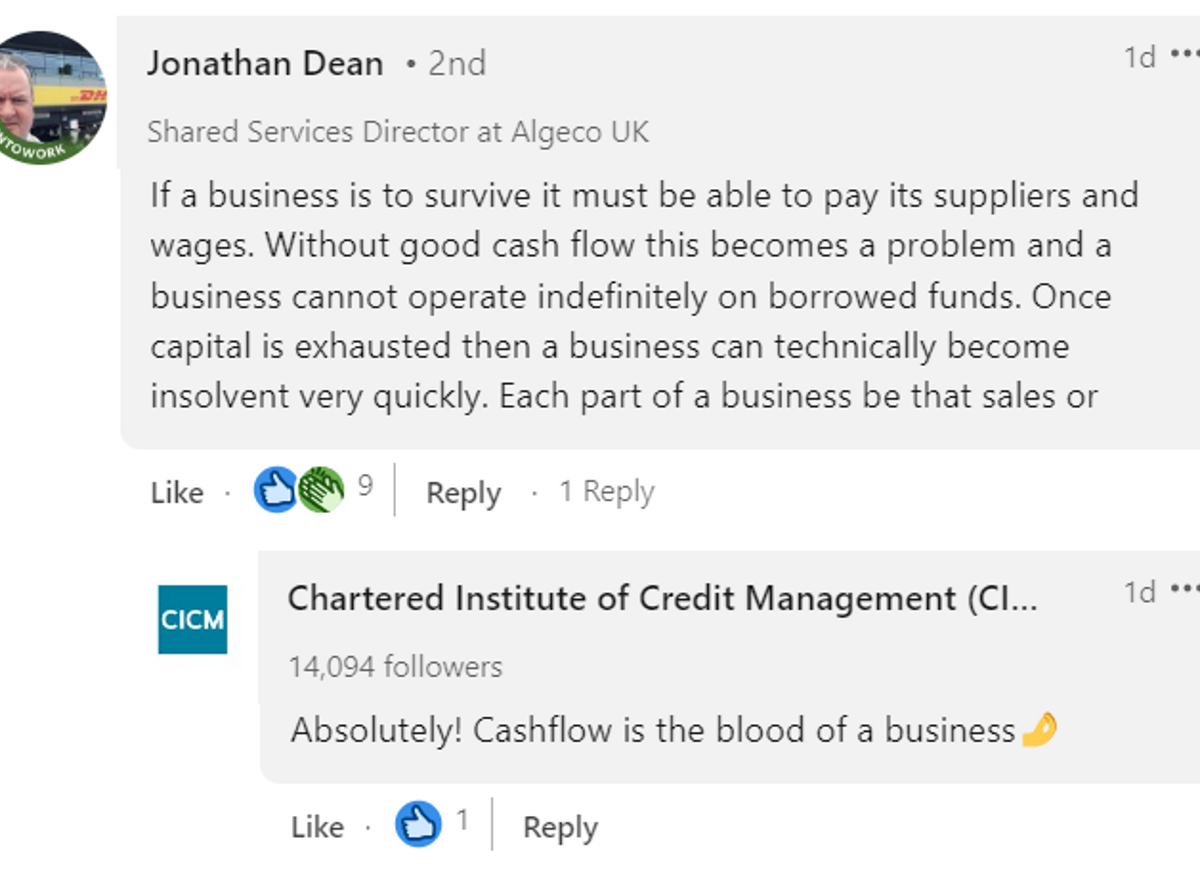

Jonathan Dean

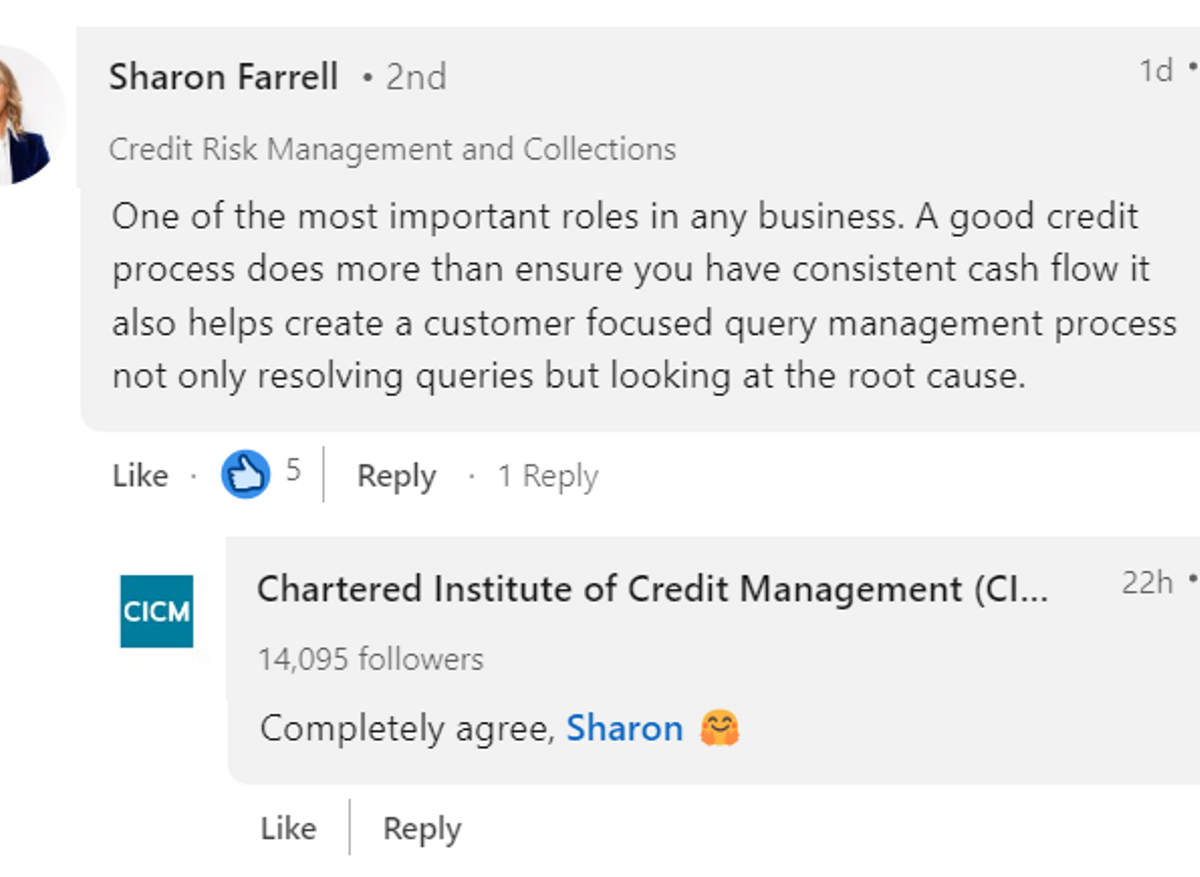

Sharon Farrell

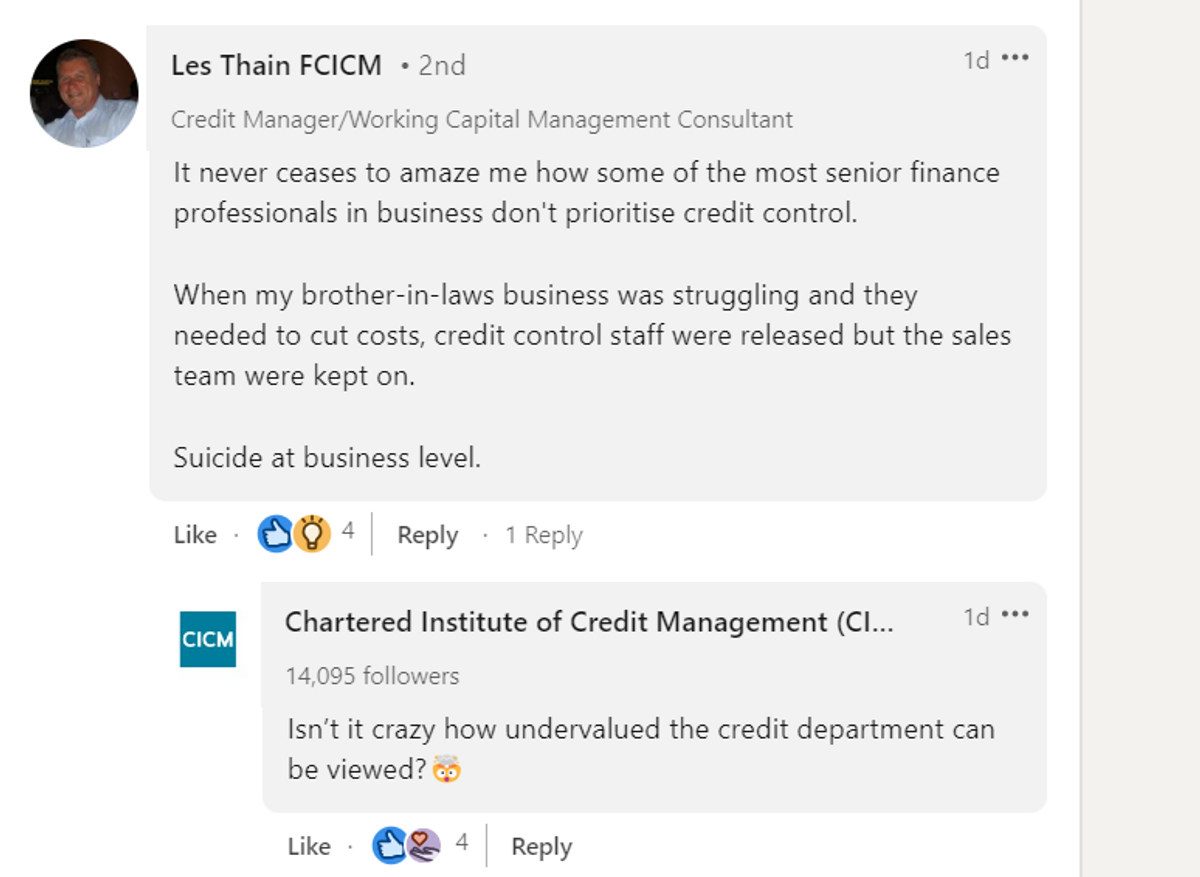

Les Thain MCICM

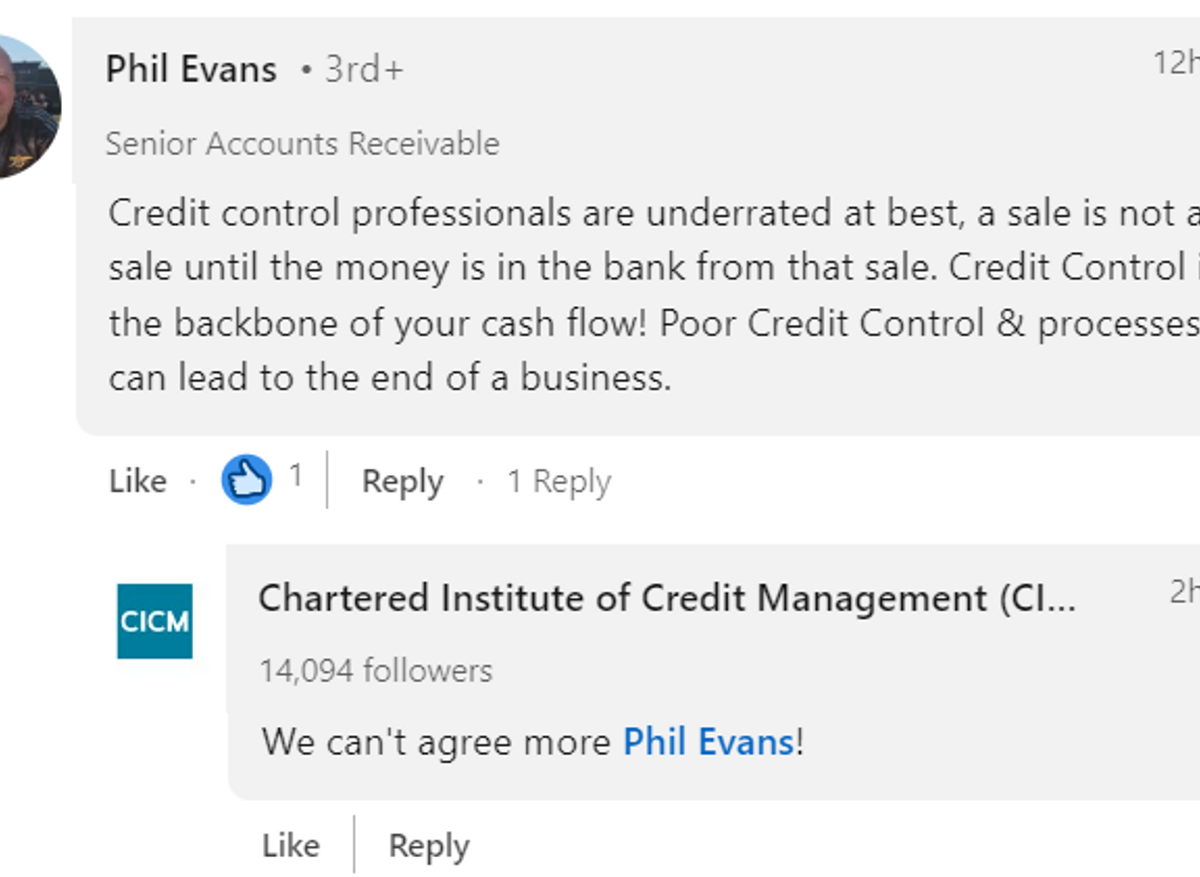

Phil Evans

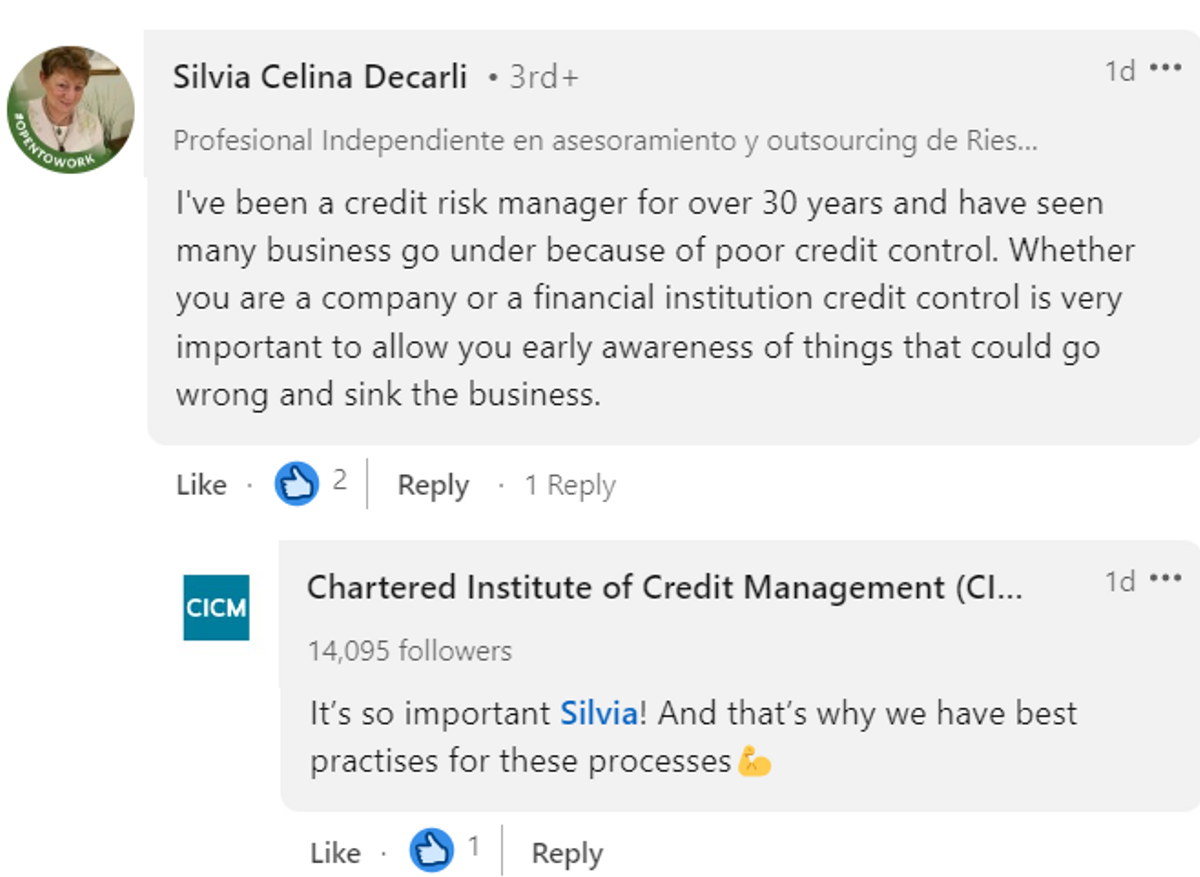

Silvia Decarli

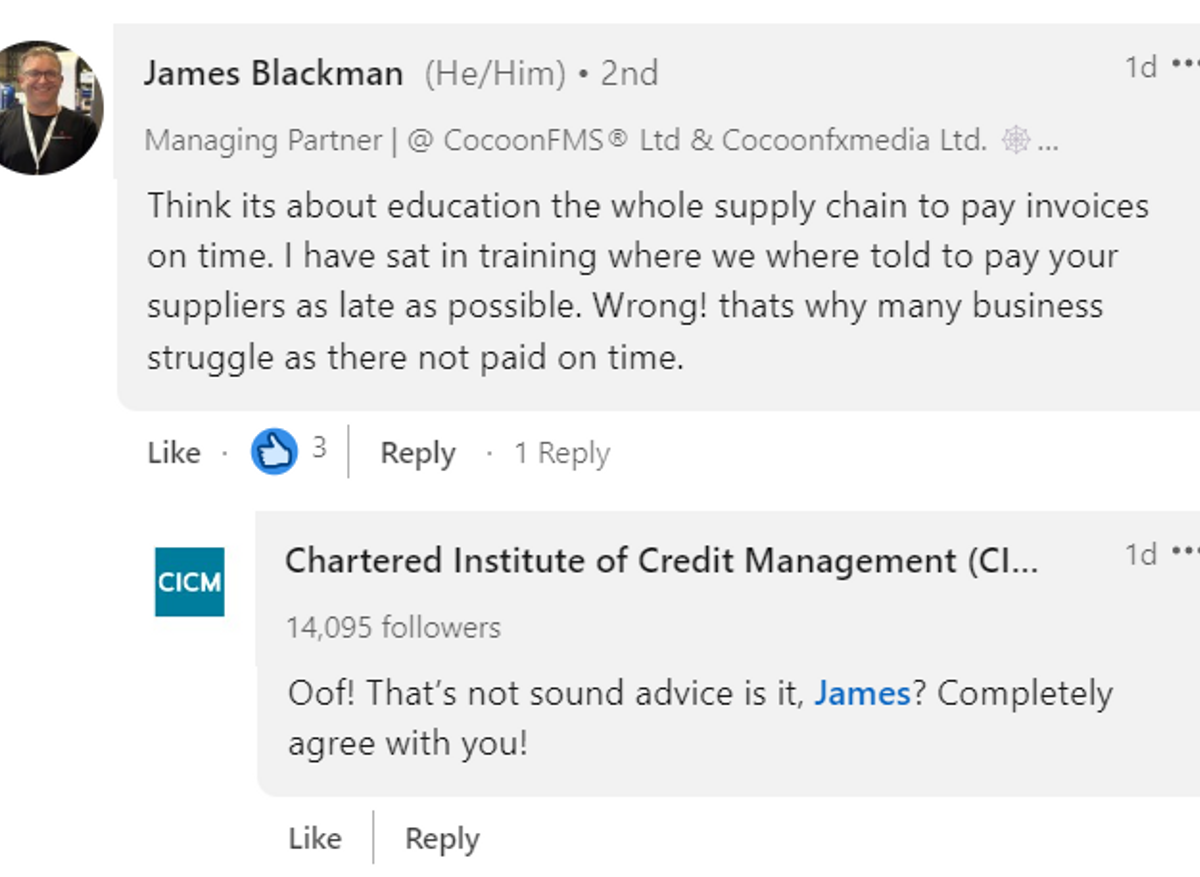

James Blackman

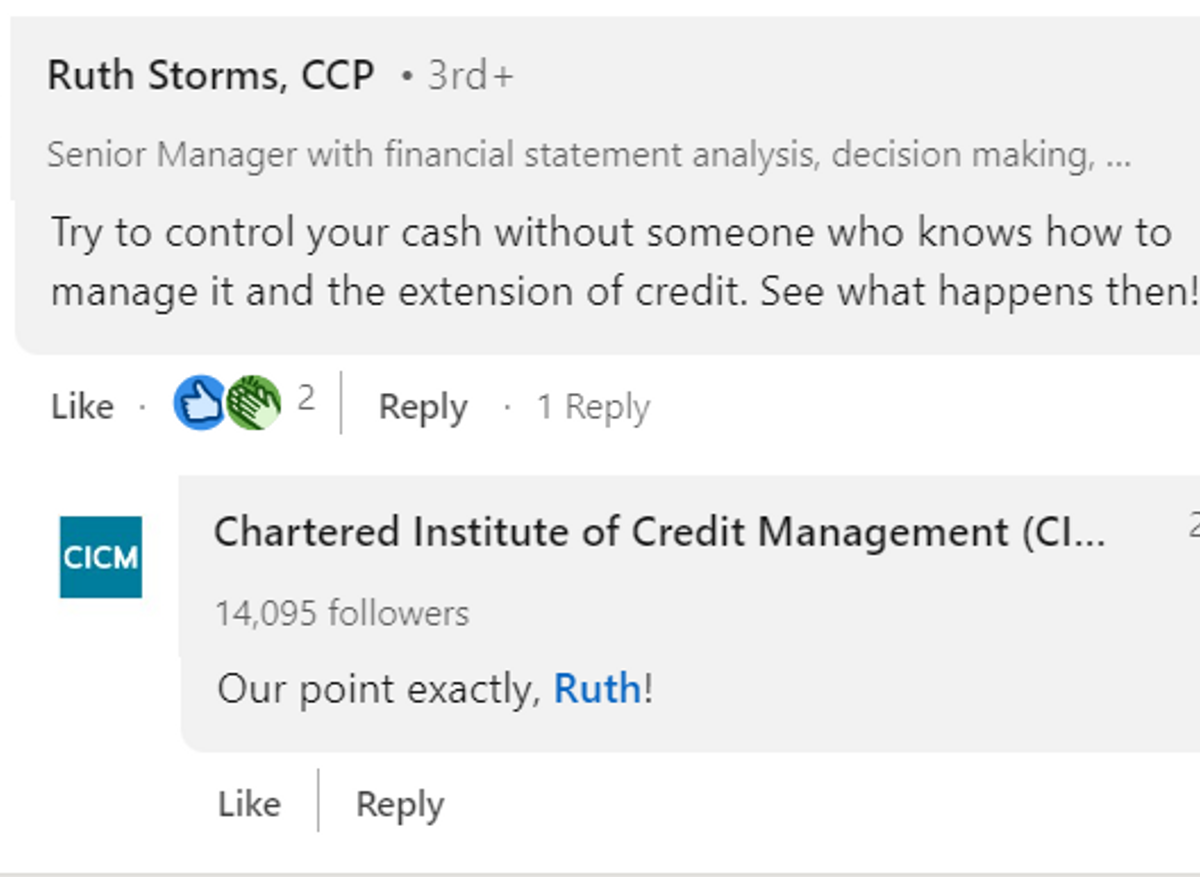

Ruth Storms

Why Credit Control is important

Let's dive into our list of reasons why Credit Control is important.

Mitigate financial risk

Credit control can be seen as a protective service – a shield against Credit Risk.

Vetting and onboarding customers

At the beginning of the customer relationship, during the vetting and onboarding stage, the Credit Control function begins. It helps to avoid legal complications arising later in the cycle by making sure the customer’s legal identity is properly recorded and that all relevant Terms and Conditions of Sale have been provided.

Risk Assessment

The next important consideration –is risk assessment. This involves understanding the customer’s creditworthiness and their affordability, or ability to pay. Higher risk customers are identified as part of the customer due diligence process, so that appropriate measures are put in place to protect against the increased risk of slow and non-payment. These could include offering a reduced credit limit, operating on shorter payment terms or obtaining some form of security.

Even at the earliest stages of the customer relationship, effective Credit Control can help identify and manage warning signs which could otherwise prove costly through losses to bad debts and a hit to business profits.

The most significant asset of a business is likely to be its Accounts Receivable ledger, and as we’ve seen the essential role of Credit Control is protecting that investment. However, it’s no good having working capital locked up in a ledger – it needs to be released and converted to cash as quickly as possible! Having skilled collectors who know how to collect the cash is essential in allowing you’re a business to meet its financial obligations, invest in growth and maintain a competitive edge.

Grow Customer Relationships

Customers are a top priority. In credit control, there is a need to foster and nurture relationships. When customers get a seamless experience and service that looks after them, they’re going to trust the organisation’s people even more. That leads to repeat business customers and positive word-of-mouth.

We must remember that customers are human. Automation is great but it’s easy to forget the impact of the human touch so a successful Credit Control function will make sure this human element is retained this in their processes.